Economic and Market Update - January 2022

January 31, 2022

- Tensions in Ukraine have risen as Russia threatens to invade Ukraine. The U.S. and other allies to Ukraine have discussed imposing sanctions on Russia in order to discourage an invasion, however potential for military conflict remains.

- The U.S. Economy grew at a 6.9% annual rate in the 4th quarter, well above consensus of 5.8%. The strength reflected a rebound in activity after the Delta variant surge which constrained growth in the 3rd quarter.

- Following the Federal Reserve meeting in January, Chairman Powell’s comments continue to point to the possibility of a more aggressive rate hiking schedule, with markets now pricing in potentially up to five 0.25% hikes through 2022.

- Movement in interest rates have picked up, with the 10 Year Treasury yield rising from ~1.63% to start 2022 up to nearly 1.90% in the 3rd week of January.

- This precipitated volatility in the stock market, as higher borrowing costs, among other factors, can negatively impact company earnings. The S&P 500 and NASDAQ indices have fallen -9.80% and -15.51% respectively from their peaks.

- Cryptocurrencies, often looked to as an asset class less correlated with stocks and bonds, have struggled as well, with Bitcoin falling from its peak in November by roughly 50%. The volatility in part could be attributed to rumors of the U.S. government planning to regulate the digital asset space.

In evaluating economic data relative to expectations, more releases have missed expectations through December as the Omicron variant slowed down consumer and business activity. However, in Europe where Omicron cases spread and subsequently peaked earlier than in the U.S., data has already begun to surprise to the upside again. Expectations are for the U.S. to follow the same pattern as case counts subside.

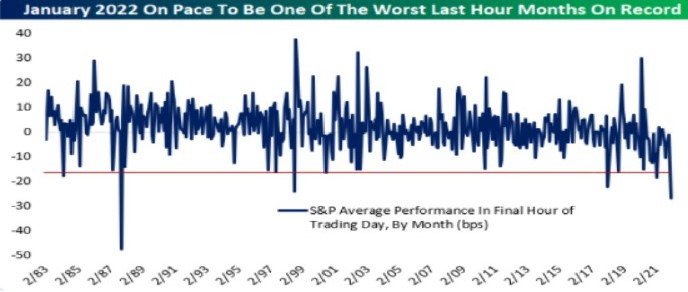

The movement of stock prices during the last hour of the trading day is often watched as an indicator of how large institutions are trading. The belief is that institutions trade more in the final hour after monitoring the entire day’s price action. January is on pace to be the worst month of final hour trading (i.e. more selling in final hour) since 1987. This indicates bearish sentiment remains as investors look for a market bottom.

A number of forces are contributing to the rocky start for markets in 2022. Uncertainty around COVID-19, corporate earnings, inflation, and geopolitical risks with Russia have played a part. The Federal Reserve’s monetary policy moves though, seem to be having an outsized effect on market volatility. Specifically, over the past few months the Fed’s rhetoric has shifted to a more aggressive tone in raising interest rates. Over that period, the market has gone from expecting the first 0.25% hike to not happen until May or June 2022, to now pricing in expectations of at least a 0.25% (potentially even 0.50%) rate hike in March and up to 5 total hikes through the year. As a result, bond and stock prices have been pressured. So far, the S&P 500 hasn’t officially experienced a ‘correction’, defined by a decline of -10%, but a decline of that magnitude should not come as a surprise given market history. On average, declines of -10% or more happen at least once every 19 months. The market fell roughly that amount (–9.60%) in September 2020, meaning this decline is fairly normal, at least from a frequency standpoint. Although interest rate movement has induced some volatility, since 1962 the S&P 500 has produced positive returns in periods where the 10 Year Treasury yield is rising 78% of the time. The market’s path has gotten off to a bumpy start, but the leading economic data and analysts’ earnings estimates indicate that the economy and stock market can continue to grow.

The purpose of the update is to share some of our current views and research. Although we make every effort to be accurate in our content, the datum is derived from other sources. While we believe these sources to be reliable, we cannot guarantee their validity. Charts and tables shown above are for informational purposes, and are not recommendations for investment in any specific security.

Categories

Contact A Wealth Advisor Today